Navigating the Shift: Why Ford’s Focus on Profit Power is Key to Ford Stock Performance

The automotive industry is in the midst of a once-in-a-generation transformation, and for investors tracking Ford stock (NYSE:F), the company’s recent strategic maneuvers are painting a clearer picture of its path to sustainable profitability. In a decisive pivot that prioritizes financial stability and core market strength over rapid, loss-making electric vehicle (EV) expansion, Ford is doubling down on its most profitable assets: the iconic F-Series trucks. This calculated shift, driven by a combination of strong traditional demand and unexpected supply chain shocks, highlights a mature, pragmatic approach to navigating a volatile market.

The F-Series: Ford’s Profit Engine Drives New Strategy

Ford’s financial backbone has always been its F-Series lineup, which includes the perennial best-selling F-150 and the heavy-duty Super Duty trucks. This segment generates the overwhelming majority of the company’s profits, an essential fact for understanding the movements of Ford stock.

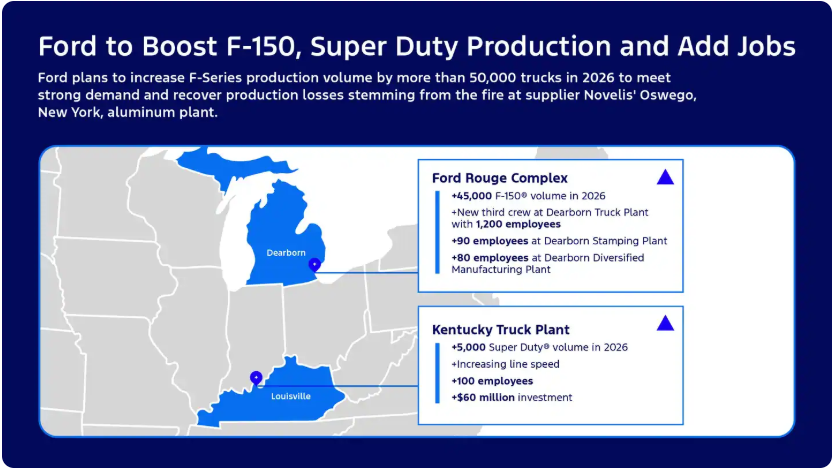

In a direct response to both soaring customer demand and the need to recover lost production, Ford has announced a significant boost to F-Series production. The company plans to add a third crew at the Ford Rouge Complex in Dearborn and enhance output at the Kentucky Truck Plant. This massive operational expansion will add over 50,000 trucks annually—45,000 in Dearborn and 5,000 in Kentucky—with the new units starting to roll off the lines in the first quarter of 2026.

This strategic expansion is about more than just volume; it’s about shoring up the company’s financial resilience.

Mitigating the Aluminum Crisis

The production ramp-up is particularly critical given the unexpected hit Ford absorbed from a September fire at the Novelis aluminum plant in Oswego, New York. This disruption to a key supplier of aluminum, a material central to the lightweight construction of the F-Series, resulted in a substantial production loss. Ford reported this loss translated into a staggering $1.5- to $2-billion profit hit in its third-quarter earnings, forcing the company to lower its full-year earnings guidance.

By adding over 1,000 new jobs and dedicating significant resources to increased F-Series output, Ford is actively working to mitigate the long-term effects of this supply chain shock. Company executives believe this recovery plan will allow them to offset at least $1 billion of the Novelis-related financial adjustments in 2026. The ability to rapidly mobilize its manufacturing might to overcome such a hurdle demonstrates a key competitive advantage that investors should weigh when evaluating Ford stock.

Financial Resilience and Market Reaction

Despite the supply chain setback, Ford’s overall financial health appears robust. The company reported a solid third-quarter net income of $2.4 billion, a significant jump from $900 million a year prior. Adjusted income stood at $2.6 billion, and revenue soared by 9% to a record $50.5 billion.

The earnings report, while clouded by the one-time Novalis impact, showcased the underlying strength of the Ford Blue (traditional vehicles) and Ford Pro (commercial) divisions, which continue to deliver healthy profit margins. The market’s reaction to Ford’s mixed guidance—a strong performance beat countered by a lowered full-year outlook due to the fire—was initially cautious, but the stock’s resilience reflects investor confidence in the company’s core business and long-term recovery plan. Analysts have noted that without the one-time fire expense, Ford’s performance would have pushed its guidance above the original range, underscoring the health of its operations.

A lower-than-anticipated tariff impact—estimated at $1 billion, roughly half of original projections—provides a small tailwind, but the primary narrative for Ford stock remains its strategic focus on high-margin vehicles.

The Electric Vehicle Pivot: Pragmatism Over Pace

Perhaps the most telling aspect of Ford’s new direction is the recalibration of its EV strategy, a move that has direct implications for its capital expenditure and future profitability—two core drivers of Ford stock valuation. The company has announced an indefinite pause in the production of the F-150 Lightning electric pickup, with the roughly 500 workers from the idled Rouge Electric Vehicle Center being transferred to the Dearborn Truck Plant to build gas-powered and hybrid F-Series trucks.

This decision is driven by a stark financial reality: the gas-powered and hybrid trucks are currently “more profitable” for Ford and use less aluminum, simplifying their supply chain.

CEO Farley’s Outlook and the Hybrid Bridge

Ford Motor Co. CEO Jim Farley has become a leading voice advocating for a more measured approach to the EV transition. During the third-quarter earnings call, he presented a cautious outlook on immediate EV adoption in the U.S. market, predicting that EV adoption in the near term will settle at around 5% of the U.S. market. This significant downward revision challenges the hyper-aggressive EV forecasts that have recently pressured traditional automakers.

Farley’s strategy is not an abandonment of the electric future but a tactical pivot towards profitability. The focus is shifting to Hybrid and ICE-powered vehicles as a crucial bridge.

Simultaneously, Ford is laying the groundwork for a more affordable, profitable EV future. Farley touted Ford’s new Universal EV platform, designed to underpin “digitally advanced, very spacious, and appealing products that start at around $30,000.” By sourcing 95% of the EV’s components and kicking off production of LFP battery cells at the BlueOval Battery Park in Marshall, Michigan, Ford is aggressively working to drive down the enormous costs associated with its Model e division, which has been reporting significant losses. This focus on cost-efficient, mass-market EVs is a sensible strategy to prepare for future demand without bleeding cash in the present.

Competitive Landscape and Investor Takeaway

Ford’s pivot is not occurring in a vacuum. Major rival General Motors (NYSE:GM) is also scaling back its EV ambitions, halting production of the BrightDrop EV Fleet van and citing a “significant pullback” in EV demand. This industry-wide reassessment confirms that the initial hyper-growth phase of the EV market has matured, and profitability is now the priority.

For investors, the long-term outlook for Ford stock rests on the successful execution of this dual strategy:

- Maximizing Core Profit: Leveraging the immense demand and high margins of the F-Series, Ford Blue, and Ford Pro segments to generate robust cash flow and fund future investments. The production boost of 50,000 trucks is a clear signal of this commitment.

- Disciplined EV Development: Shifting from a volume-at-any-cost model to a profit-focused approach in the Model e division, particularly by delaying the F-150 Lightning and developing the Universal EV platform for affordable models.

The decision to pause the Lightning is a short-term sacrifice of EV market share for long-term financial health. The reallocation of resources to build more profitable gas and hybrid F-Series trucks is a pragmatic move that is expected to generate significant shareholder value, proving that in today’s auto market, profit power is paramount to a healthy Ford stock valuation. As the company steers through supply disruptions and a challenging EV adoption curve, its focus on its iconic, high-margin trucks provides a necessary foundation for enduring success.

#FordStock #FSeries #FordF150 #EVs #AutoIndustry #JimFarley #Investing #Ford